R-Multiples and Expectancy

A Primer on What to Expect From Your Trades

Expectancy in trading refers to the average R-multiple that a trading system generates over a series of trades. An R-multiple is a way of expressing profits and losses as a multiple of the initial risk taken on a trade (R, as R=Risk). The late Dr. Tharp has written a lot about this, and his books rank among my all time favorites.

Systematic traders tend to consider risk-reward ratios prior to taking a trade. This involves determining the risk budget of a trade by setting an exit point (stop) to limit losses and preserve capital. The distance between the entry price and the exit point represents the R, or the expected loss for that trade.

For instance, if a trader buys one WTI crude oil futures contract at $100 and sets a stop at $90, the risk (R) would be $10,000 per contract as the contract’s multiplier is $1,000.

Personally, I use ATRs (average true ranges) to set stop levels, which then determines my R. This method connects Rs to ATRs and allows me to analyze all my trade statistics in R and ATR terms, which I find really useful.

Returning to our example, if the trader makes a profit of $20,000, that’s a 2R trade because the trade has earned twice the initial risk. On the other hand, a loss of $5,000 would be a 0.5R loss.

A backtest allows us to view the P&L of each trade as a multiple of the initial R — an R-multiple distribution. The average R-multiple of this distribution is our expectancy per trade.

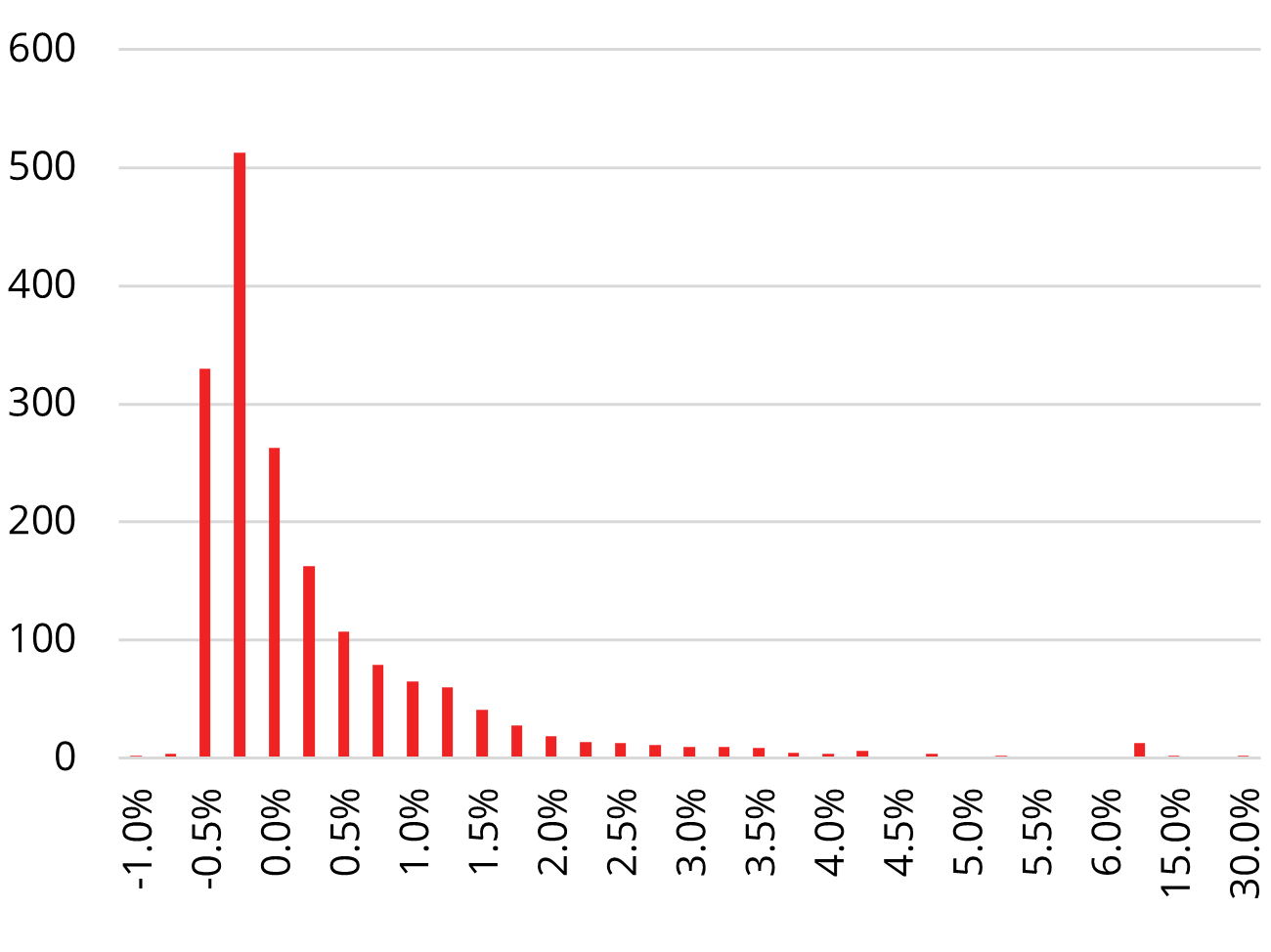

Here’s a chart from the Takahē Systematic Trend program which translates the R-multiple into a percentage P&L. The -0.5% point is 1R.

The chart shows that most trades are small losing trades with a loss between 1R and 0R (-0.5% to 0%). However, our R-multiple distribution is positively skewed as the Takahē Systematic Trend program is designed to cling to the occasional outlier price move which make the trade earn multiples of the initial risk, e.g., 10R or more. The average R is around 0.4, and this is our expectancy per trade.

One of the most important factors for trading success is to keep losses small. Keeping losses at 1R or less is paramount. Don’t overthink it: If a trade has consumed its risk budget, get out. You can always get back in.

Another important aspect is sample size. In our view, R-multiple distributions need to be based on hundreds, if not thousands, of trades in order to be meaningful. This means that systematic traders should design their systems so that they can actually produce a meaningful sample size. Usually, the more bells and whistles one includes, the smaller the sample size and the more fragile the system. The aim should be to design resilient systems which, when operated for the long-haul, have significant statistical odds of making money.

In this game of numbers and odds, many single trades will lose money, and although the above distribution of trade results looks attractive, most people prefer environments in which they are right more often than they are wrong. It simply “feels” better, however, it’s a mistake as far as good trading is concerned since most “feel good” systems tend to have negative overall expectancy. In the Takahē Systematic Trend program, we’re right only 30-40% of the time, but the R-multiples are skewed in our favor and drive our system’s overall positive expectancy.

Well thought out!